An Executors Guide to Compensation

Navigating the complexities of estate administration can be a daunting task, often requiring a significant investment of time and effort. In Alberta, the role of an Executor or Administrator of an Estate (“Personal Representative”) often demands considerable obligations as the person tasked with managing and finalizing the Estate. Additionally, the role can expose the Personal Representative to personal liability in various instances. As such, Executors are entitled to charge the Estate a reasonable executor fee to compensate them for their contributions.

The Surrogate Rules outline the fundamental rules for Personal Representative Compensation but do not specify an amount or set a flat fee. Instead, the Surrogate Rules state that Personal Representatives must receive “fair and reasonable compensation” for their responsibility in administering an Estate and set out factors to be considered in determining such compensation.[1]

As such, when determining what is fair and reasonable compensation for Personal Representatives, the following should be considered:

- Is the compensation fixed in the Will?

- What is the range for compensation under the Suggested Fee Guidelines (the “Guidelines”)?

- What is “fair and reasonable” compensation considering the factors set out in the Surrogate Rules?

SIDE NOTE ON OUT-OF-POCKET EXPENSES

Personal Representatives might expend their own money for estate expenses while they are administering the estate. They are entitled to reimbursement for these reasonable out-of-pocket expenses. Reimbursable expenses may include professional fees, postage, property managers, insurance, etc. It is important to keep receipts for all expenses incurred as a Personal Representative to present to the Estate for reimbursement.

FIXED COMPENSATION

If compensation is set out in the Will as a fixed amount or percentage, the Personal Representative cannot seek a greater amount unless they have the agreement of the beneficiaries to vary the fixed amount or they receive Court approval to vary.[2]

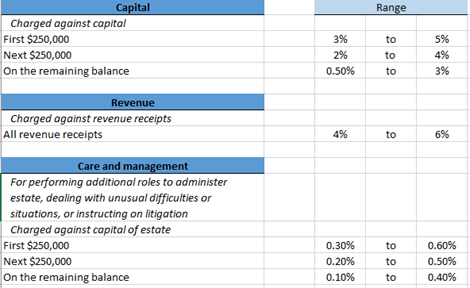

SUGGESTED FEE GUIDELINES

If the Will is silent on any fixed compensation or if there is no valid Will, a Personal Representative can propose compensation subject to the approval of the beneficiaries or the Court. The Court will often refer to the Suggested Fee Guidelines (“Guidelines”) as a starting point to determine fair and reasonable compensation. As such, it makes sense for Personal Representatives to also use the Guidelines as a starting point for their proposed compensation. The Guidelines are comprised of 3 categories, with different rate brackets in 2 of these categories.

The categories are (1) Capital, (2) Receipts & Revenue, and (3) Care & Management. Personal Representatives can claim in 1 or 2 or all 3 categories. Most Personal Representatives will claim based on the “Capital” category and sometimes the “Revenue” category (if there has been income earned during the estate administration). It is not common to claim the last category unless there are extraordinary circumstances and unusual work done by the Personal Representatives.

Although the Guidelines were published in 1995, they continue to be referenced by the Court in current day.

SURROGATE RULES: FACTORS FOR COMPENSATION

Once a range is calculated using the Guidelines, the Personal Representative will typically propose an amount within the range. Whether the proposal is on the higher or lower end of the range is based on the specific circumstances of the Estate. The Court will consider the factors set out in the Surrogate Rules under Schedule 1 in determining what is fair and reasonable, therefore the Personal Representative should consider the same factors when proposing higher or lower compensation. The factors are:

- The gross value of the Estate;

- The amount of revenue receipts and disbursements;

- The complexity of the work involved and whether any difficult or unusual questions were raised;

- The amount of skill, labour, responsibility, technological support, and specialized knowledge required;

- The time expended;

- The number and complexity of tasks delegated to others;

- The number of personal representatives appointed in the will, if any.

There are some situations that may justify additional compensation, such as in the Care & Management category:

- Where the Personal Representative is called upon to perform additional roles in order to administer the Estate, such as exercising the powers of a manager or director of a company or business;

- They encounter unusual difficulties or situations; or

- They must instruct a lawyer on litigation related to the administration of the Estate

The Court has discretion to increase or reduce the amount of compensation depending on the circumstances of each Estate.

Where there is more than one Personal Representative, the compensation is claimed on a joint basis and shared equally unless the Personal Representatives have agreed to different allocation amongst themselves.

PERSONAL REPRESENTATIVE COMPENSATION & TAXES

Personal Representative compensation is considered taxable employment income and therefore subject to income tax and payroll remittances, including CPP, EI, etc. Reimbursement for out-of-pocket expenses is not considered income and would not be subject to income tax or remittance withholdings.

If you are a Personal Representative and have any questions related to your Personal Representative compensation entitlements or the estate administration process, please contact a member of our Estates & Trusts practice group.